Chinese

Chinese Russian

Russian Arabic

Arabic

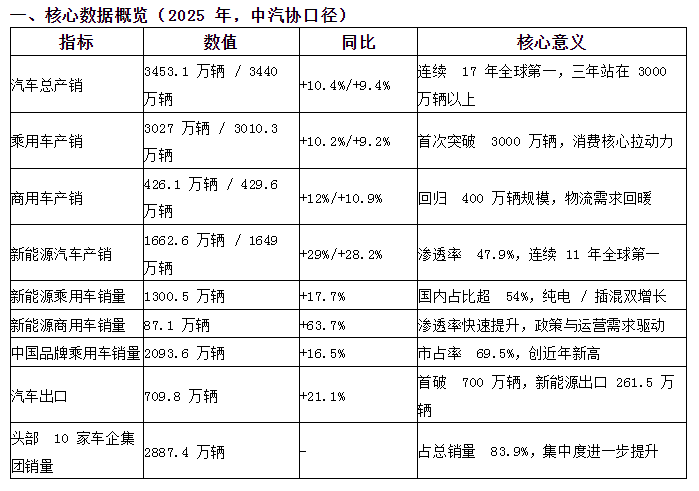

In 2025, China's automobile market will end with production and sales exceeding 34 million units, new energy penetration rate of nearly 50%, independent market share of nearly 70%, and exports exceeding 7 million units for the first time, showing the core characteristics of "reaching a new high in scale, accelerating structural upgrading, and reshaping the competitive landscape". At the same time, it also faces challenges such as pressure on profits, intensified price wars, and differentiation of technical routes. The following is a collation, analysis and summary based on data from authoritative organizations such as the China Automobile Association.

2. In-depth analysis of core data

1. Scale and structure: New energy is dominant, and fuel vehicles are accelerating their shrinking

·New energy vehicles: Production and sales of 16.49 million units, with a penetration rate of 47.9%(reaching 52.3% in December), and domestic sales of 13.875 million units, a year-on-year + 19.8%. For the first time, it surpassed traditional fuel vehicles in the domestic market; pure electricity and plug-in hybrid growth in parallel, fuel cells are growing rapidly under a low base, and the technical route has shifted from single to diversified.

·Traditional fuel vehicles: Domestic sales were 11.06 million units, a year-on-year- 4.3%. The share continued to be squeezed, and joint venture brands were under significant pressure (for example, Honda's annual sales were 645,000 units, a year-on-year- 24.28%).

·Passenger car segmentation: SUVs account for about 50%, sedans account for about 46%, MPV growth is accelerating, new energy MPV and off-road vehicle models have become new hot spots; intelligent driving is accelerating penetration, and the proportion of new cars with combined driving assistance accounts for more than 60%.

2. Competitive landscape: Independent and strong rise, joint venture share declines, new forces diverge

·Self-owned brands: The market share is 69.5%, an increase of 4.3 percentage points from 2024. BYD (4.602 million vehicles), SAIC (4.507 million vehicles), Geely (3.024 million vehicles), Chang 'an (2.913 million vehicles), and Chery (2.8064 million vehicles) lead the way. Geely Galaxy's annual sales exceed one million, and Changan's new energy growth rate exceeds 50%.

·Joint venture brands: Share continues to decline, and German/Japanese/American brands are facing pressure. Some brands are trying to break through through electrification transformation and localized R & D, but the overall pace lags behind.

·New forces in car-building: Zero running vehicles (596,600 vehicles,+103%), Xiaomi Automobile, etc. have achieved high growth, and zero-running vehicles are expected to make annual profits; Weilai, Xiaopeng, etc. have grown steadily, collectively impacting the profit turning point.

3. Globalization and industrial chain: export volume and price are rising, and supply chain is independently controllable

·Export scale: 7.098 million units, year-on-year + 21.1%. New energy exports were 2.615 million units, accounting for more than 36%. Europe, Southeast Asia, and the Middle East have become core markets. China brands have moved from "going global" to "going in," and overseas factories and localized operations have accelerated.

·Industrial chain: Large computing power chips and intelligent wire-controlled chassis are on board in batches. The autonomy rate of core components such as batteries, motors, and electronic controls exceeds 90%. The cost advantage is consolidated, but there are still shortcomings in chips, high-end sensors and other fields.

4. Growth drivers and constraints

·Driving factors: policy continuation (purchase tax exemptions, trade-in for old ones), abundant supply (explosion of new energy models), improved infrastructure (more than 8 million charging piles), high export growth, and consumption upgrades (increased demand for smart/luxury).

·Constraints: Price wars have put pressure on industry profits, and some automobile companies have widened losses; new energy growth has slowed down, shifting from "inclusive growth" to "head concentration"; technological route differentiation (solid state batteries, hydrogen fuel cells, hybrid technology) has intensified investment in R & D and supply chain; overseas trade barriers (such as EU countervailing investigations) have increased export uncertainty.

3. Core conclusions

1. Scale and status: China's global dominant position in the automobile market has been consolidated, and the scale of production, sales and exports continues to expand. However,"big but not strong" still exists-no car company has annual sales of more than 5 million vehicles, and no car company with strong appeal and brand premium in the world is still far from being an international giant. Although it occupies a strong position at home, it still belongs to the stage of "rural areas surrounding cities" overseas.

2. Structural transformation: Electrification has entered a period of large-scale popularization, and intelligence has become the focus of new competition. The penetration rate of new energy may decline in 2026 (subject to factors such as the decline of purchase tax subsidies), and the coexistence of multiple routes such as pure electricity/plug-in hybrid/extended range/hydrogen energy will continue.

3. Competitive landscape: Independent and new forces dominate the incremental market, joint venture brands accelerate electrification and localization, star models have a short life cycle (competition intensifies, iteration speeds become faster); head concentration has increased, the survival pressure of small and medium-sized car companies has increased, and the integration of mergers and acquisitions in the industry is accelerating.

4. Profitability and quality: The industry has shifted from "fighting for scale" to "fighting for value". Technological innovation, brand advancement, and cost control have become the keys to profit. Export and high-end are the core paths to improve profits. 5. Risk warning: Price wars, raw material fluctuations, trade frictions, and technology iteration risks need to be vigilant. Enterprises need to balance scale expansion with profit quality to avoid low-level duplication of construction.

Source: Hou Ge's work insights

[Disclaimer] The content of this website (including pictures and texts) originates from the Internet, and the copyright belongs to the original author. Respect the rights and interests of originality, and select content is only used for information sharing. If copyright disputes are involved, please contact us to handle the deletion in a timely manner.

Online Evaluation

Online Evaluation I am Buyer

I am Buyer Export Services

Export Services subsites

subsites

023-62852688

023-62852688  No. 1-1, No. 2899, Longzhou Avenue, Banan District, Chongqing City

No. 1-1, No. 2899, Longzhou Avenue, Banan District, Chongqing City

Headquarters

Headquarters